The first step to buying a house is financing, which means that lenders need to know all about your finances before approving you for a loan. This is done by getting your credit score. The importance of this score has been widely publicized, and the consequences for having one that’s too low or even negative have been made abundantly clear by credit monitoring services. Here is how a bad credit score will affect your mortgage rates.

Why lenders care about credit scores

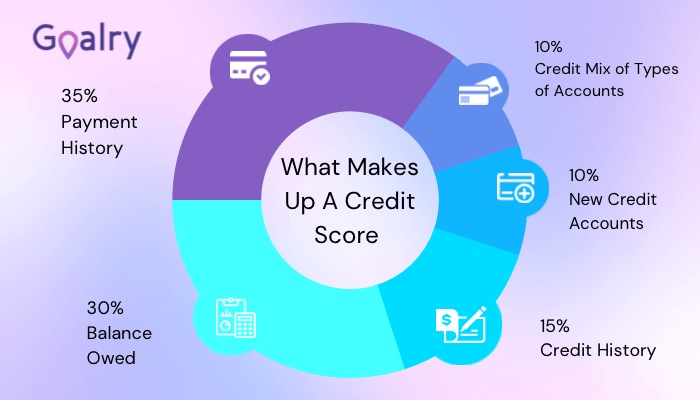

The first thing to answer how your credit score will affect your mortgage rates is knowing why lenders care about the credit score. A credit score is a number that lenders like banks use to determine whether or not they will approve your request for credit. The higher the number, the more likely you are to be approved for loans and other types of credit. Lenders use credit monitoring systems to calculate this score.

Credit scores are based on your credit record. Your credit report is based on your credit history, built up over time as you take out loans and handle them responsibly by making the agreed-upon minimum payments each month. Therefore, if you have a bad credit score, it means you are highly likely to default on a loan, and a lender would be hesitant to lend you a huge amount for buying a house mortgage.

The range for credit scores

The FICO credit scores range between 300 and 850, where 300 is considered the lowest while 850 is the highest. Here is an outline of how these credit scores are divided. This information will help you know how much you need to work on your credit score.

800 (Exceptional)

740-799 (Very Good)

670-739 (Good)

580-669 (Fair)

Below 580 (Poor)

A high credit score indicates that individuals pay their loans on time and never default. A low credit score means that an individual does not pay their loans on time and is likely to default.

How they affect mortgage rates

You might not buy your preferred house

When getting a mortgage, an underwriter would evaluate the mortgage application to assess your ability to pay the monthly amount. The underwriter will provide you with cheaper options that might not match your ideal home. However, if you have a good credit score, it means you can afford your most preferred house because the lender is confident that your credit record will facilitate timely payments. If you have a bad score, you are likely to default on your mortgage repayment, which lowers your chances of getting a good mortgage rate.

Higher mortgage rates

The rates charged on mortgages vary from one credit score to another. People with a high credit score would pay a lower interest rate than an individual with a poor credit score. This means that a person with a low credit score is more exposed to risk than a person with a high credit score. The more interest rate a person is required to pay, the more challenging it is for them to take the offer.

Do all mortgages consider credit scores?

This is a question that many people with a low credit score tend to ask. The good news is that some mortgage options focus less on an individual’s credit score. This means that the individual can get a low-interest loan to buy their preferred home regardless of their credit score. If you are unsure how to get the best lending option in the market, it is advisable to work with companies that provide loans to people with poor credit scores. You can find one on Loanry.com.

Your credit score is an important aspect of your life because it will also affect your ability to get other loans. If you want to get favorable mortgage rates, it is advisable to work on your credit score before applying for your mortgage. Once your credit score has risen, you can be assured of getting favorable mortgage rates. Such can be achieved by taking loans and repaying them on time or making new agreements with the lender.